by Robyn Bolton | Mar 25, 2026 | AI, Leadership, Strategy

“AI is the new cigarette.”

When a colleague said this in the waning days of 2022, days after ChatGPT burst on the scene, she took my breath away. The idea that this miracle would kill us seemed confined to hysterical handwringing foretelling the birth of Skynet.

She was right.

But neither of us knew it was designed to be that way.

Designed for addiction

My friend predicted that ChatGPT would stay free and helpful until usage reached “critical mass,” and then we’d have to pay. Less than three months after its November launch, OpenAI introduced its $20 per month service.

But it’s not the “first one’s free, the next one will cost you” aspect of drugs that makes AI addictive. It’s the design decisions at its core that keeps you coming back:

- Purchase Decoupling in which you convert real money into tokens, creating psychological distance between you and your actual spending

- Difficulty Curve where skills and benefits accumulate quickly giving you the sense that you’re becoming more capable over time and therefore more committed after progress slows.

- Skill Atrophy where every skill you stop practicing because the machine does it for you, quietly disappears.

Even casual AI users have experienced one or more of these:

- You get a message mid-chat telling you you’ve used all your tokens and need to come back in three hours even though you’ve paid your monthly $20 fee

- You’re prompting in all caps because it’s the only way you can think of to get the LLM to stop hallucinating, while reminiscing about the days when it was a brilliant thought-partner

- You’ve relied on AI to outline articles for the last several months, but you need to write in a different style and have no idea how to get started.

And yet, we keep going back.

But it’s not just individuals who are addicted. It’s entire organizations.

Signs that your organization is addicted to AI

Your CFO asks for the total AI spend across the organization. Three weeks and four departments later, the number is three times what anyone expected because the licenses are buried in IT infrastructure budgets, the pilots are expensed as innovation projects, and half the tools were purchased by business units on corporate cards.

The board approved the AI transformation initiative based on the pilot results. Eighteen months later, the pilot case study slide hasn’t changed, headcount has been reduced in anticipation of productivity gains that haven’t materialized, and the team running the pilot has quietly moved on to other work.

You eliminated the analyst pool two years ago because AI could do in minutes what they did in days. Now you need to evaluate whether the AI’s output is actually correct, and you’ve just realized there’s nobody left in the organization to check it because everyone who’s done it is gone.

Sound familiar? Your organization is an addict.

Recovery is possible

Addiction can’t be cured, only managed. The same is true for AI.

The road to recovery starts in a similar place: Visibility

- Centralize AI spending the way you centralize other business processes AND allow some flexibility by setting strict spending limits and clear decision-making criteria and ownership.

- Start pilots with the end in mind by establishing success metrics and scaling plans at the start of the pilot, not when it’s already in process.

- Treat certain human capabilities as strategic reserves the same way you’d treat any critical operational dependency. Before automating a function, explicitly document what judgment and expertise currently lives there, who holds it, and what it would cost to rebuild it if needed.

Unlike cigarettes or gambling, we’ve reached a point where we can’t quit AI.

But we can be aware of our addiction and we must manage it.

The first step is admitting that it’s real. And by design.

by Robyn Bolton | Feb 8, 2026 | AI, Leadership, Leading Through Uncertainty, Strategic Foresight, Strategy

In 2023, Klarna’s CEO proudly announced it had replaced 700 customer service workers with AI and that the chatbot was handling two-thirds of customer queries. Labor costs dropped and victory was declared.

By 2025, Klarna was rehiring. Customer satisfaction had tanked. The CEO admitted they “went too far,” focusing on efficiency over quality.

Like Captain Robert Scott, Klarna misjudged the circumstance it was in, applied the wrong playbook, and lost. It thought it had facts but all it has was technical specs. It made tons of assumptions about chatbots’ ability to replace human judgment and how customers would respond.

Calibrated Decision Design, a process for diagnosing your circumstances before picking a playbook, consistently proves to be a quick and necessary step to ensure success.

When you have the facts and need results ASAP: Go NOW!

General Mills, like its competitors, had been digitizing its supply chain for years and so facts based on experience and a list of the facts it needed.

To close the gap and achieve end-to-end visibility in its supply chain, it worked with Palantir to develop a digital twin of its entire supply chain. Results: 30% waste reduction, $300 million in savings, decisions that took weeks now takes hours. It proves that you don’t need all the answers to make a move, but you need to know more than you don’t.

When you have hypotheses but can’t wait for results: Discovery Planning

Morgan Stanley Wealth Management’s (MSWM) clients expect advisors to bring them bespoke advice based on mountains of analysis, and insights. But it’s impossible for any advisor to process all that data. Confident that AI could help but uncertain whether its would improve relationships or create friction, MSWM partnered with OpenAI.

Within six months, they debuted a GenAI chatbot to help Financial Advisors quickly access the firm’s IP. Document retrieval jumped from 20% to 80% and 98% now use it daily. Two years later, MSWM expanded into a meeting summary tool to summarize meetings into actionable outputs and update the CRM with notes and follow-ups. A perfect example of how a series of experiments leads to a series of successes.

When you have facts and time to achieve results: Patient Planning

Drug discovery requires patience and, while the process may be predictable, the results aren’t. That’s why pharma companies need strategies that are thoughtfully planned as they are responsive.

Lilly is doing just that by investing in its own capabilities and building an ecosystem of partners. It started by launching TuneLab, a platform offering access to AI-enabled drug discovery models based on data that Lilly spent over $1 billion developing. A month later, the pharma giant announced a partnership with NVIDIA to build the pharmaceutical industry’s most powerful AI supercomputer. Two months later, it committed over $6 billion to a new manufacturing facility in Alabama. These aren’t billion-dollar bets, they’re thoughtful investments in a long-term future that allows Lilly to learn now and stay flexible as needs and technology evolve.

When you’re making assumptions and have time to learn: Resilient Strategy

There’s no way of knowing what the global energy system will look like in 40 years. That’s why Shell’s latest scenario planning efforts resulted in three distinct scenarios, Surge, Archipelagos, and Horizon. Multiple scenarios allows the company to “explore trade-offs between energy security, economic growth and addressing carbon emissions” and build resilient strategies to recognize which one is unfolding and pivot before competitors even spot what’s happening.

Stop benchmarking. Start diagnosing.

It’s easy to feel like you’re behind when it comes to AI. But the rush to act before you know the problem and the circumstances is far more likely to make you a cautionary tale than a poster child for success.

So, stop benchmarking what competitors do and start diagnosing the circumstances you’re in, so you use the playbook you need.

by Robyn Bolton | Feb 2, 2026 | AI, Leadership, Strategic Foresight, Strategy

It was a race. And the whole world was watching.

In 1911, Captain Robert Scott set out to reach the South Pole. He’d been to Antarctica before and because of his past success, he had more funding, more expertise, and more experience. He had all the equipment needed.

Racing him to fame, fortune and glory was Norwegian Roald Amundsen. Originally heading to the North Pole, he turned around when he learned that Robert Peary had beaten him there. He had dogs and skis, equipment perfect for the Arctic but unproven in Antarctica.

Amundsen won the race, by over a month.

Scott and his crew died 11 miles from the South Pole.

When the Playbook Stops Working

Scott wasn’t guessing. He’d tested motor sledges in the Alps. He’d seen ponies work on a previous Antarctic expedition. He built a plan around the best available equipment and the general playbook that had served British expeditions for decades: horses and motors move heavy loads, so use horses and motors.

It just wasn’t right for Antarctica. The motors broke down in the cold. The ponies sank through the ice. The plan that looked solid on paper fell apart the moment it met the actual environment it had to operate in.

The same thing is happening today with AI.

For decades, when new technologies emerge, executives have followed a similarly familiar playbook: assess the opportunity, build a business case, plan the rollout, execute.

And for decades it worked. Cloud migrations and ERP implementations were architectural changes to known processes with predictable outcomes. As time went on, information grew more solid, timelines became better understood, and the playbook solidified.

AI is different. Executives are so focused on picking the right AI tools and building the right infrastructure that they aren’t thinking about what happens when they hit the ice. Even if the technology works as designed, you have no idea whether it will deliver the intended results or create a ripple of unintended consequences that paralyze your business and put egg on your face.

Diagnose Before You Prescribe

The circumstances of AI are different too, and that requires a new playbook. Make that playbooks. Picking the right playbook requires something my clients and I call Calibrated Decision Design.

We start by asking how long it will take to realize the ultimate goals of the investment. Do we need to break even this year, or is this a multi-year bet where results slowly roll in? Most teams have a sense of this, so it allows us to move quickly to the next, much harder question.

What do we know and what do we believe? This is where most teams and AI implementations fail. To seem confident and indispensable, people present hypotheses as if they are facts resulting in decisions based on a single data points or best guesses. The result is a confident decision destined to crumble.

Where you land on these two axes determines your playbook. Apply the wrong one and you’ll either waste money on over-analysis or burn through budget on premature action.

Pick from the Four Playbooks

Go NOW!: You have the facts and need results now. Stop deliberating. Execute.

Predictable Planning: You have confidence in the outcome, but the payoff takes patience. Build a flexible strategy and operational plan to stay responsive as things progress.

Discovery Planning: You need results fast, but you don’t have proof your plan will work. Run small, fast experiments before scaling anything.

Resilient Strategy: The time horizon is long and you’re short on facts. The worst thing you can do is go all in. Instead, envision multiple futures, identify early warning signs, find commonalities and prepare a strategy that can pivot.

Apply it

Which playbook are you using and which one is best for your circumstance?

by Robyn Bolton | Oct 13, 2025 | Innovation, Leading Through Uncertainty

As a kid, you’re taught that when you’re lost, stay put and wait for rescue. Most executives are following that advice right now—sitting tight amid uncertainty, hoping someone saves them from having to make hard choices and take innovation risk.

This year’s Nobel Prize winners in Economics have bad news: there is no rescue coming. Joel Mokyr, Philippe Aghion, and Peter Howitt demonstrated that disruption happens whether you participate or not. Freezing innovation investments doesn’t reduce innovation risk. It guarantees competitors destroy you while you stand still.

They also have good news: innovation follows predictable patterns based on competitive dynamics, offering a framework for making smarter investment decisions.

How We Turned Stagnation into a System for Growth

For 99.9% of human history, economic growth was essentially zero. There were occasional bursts of innovation, like the printing press, windmills, and mechanical clocks, but growth always stopped.

200 years ago, that changed. Mokyr identified that the Industrial Revolution created systems connecting two types of knowledge: Propositional knowledge (understanding why things work) and Prescriptive knowledge (practical instructions for how to execute).

Before the Industrial Revolution, these existed separately. Philosophers theorized. Artisans tinkered. Neither could build on the other’s work. But the Enlightenment created feedback loops between theory and practice allowing countries like Britain to thrive because they had people who could translate theory into commercial products.

Innovation became a system, not an accident.

Why We Need Creative Destruction

Every year in the US, 10% of companies go out of business and nearly as many are created. This phenomenon of creative destruction, where companies and jobs constantly disappear and are replaced, was identified in 1942. Fifty years later, Aghion and Howitt built a mathematical model proving its required for growth.

Their research also lays bare some hard truths:

- Creative destruction is constant and unavoidable. Cutting your innovation budget does not pause the game. It forfeits your position. Competitors are investing in R&D right now and their innovations will disrupt yours whether you participate or not.

- Competitive position predicts innovation investments. Neck-to-neck competitors invest heavily in innovation because it’s their only path to the top. Market leaders cut back and coast while laggards don’t have the funds to catch-up. Both under-invest and lose.

- Innovation creates winners and losers. Creative destruction leads to job destruction as work shifts from old products and skills to new ones. You can’t innovate and protect every job but you can (and should) help the people affected.

Ultimately, creative destruction drives sustained growth. It is painful and scary, but without it, economies and society stagnate. Ignore it at your peril. Work with it and prosper.

From Prize-winning to Revenue-generating

Even though you’re not collecting the one million Euro prize, these insights can still boost your bottom line if you:

- Connect your Why teams with your How teams. Too often, Why teams like Strategy, Innovation, and R&D, chuck the ball over the wall to the How teams in Operations, Sales, Supply Chain, and front-line operations. Instead, connect them early and often and ensure the feedback loop that drives growth

- Check your R&D and innovation investments. Are your R&D and innovation investments consistent with your strategic priorities or your competitive position? What are your investments communicating to your competitors? It’s likely that that “conserving cash” is actually coasting and ceding share.

- Invest in your people and be honest with them. Your employees aren’t dumb. They know that new technologies are going to change and eliminate jobs. Pretending that won’t happen destroys trust and creates resistance that kills innovation. Tell employees the truth early, then support them generously through transitions.

What’s Your Choice?

Playing it safe guarantees the historical default: stagnation. The 2025 Nobel Prize winners proved sustained growth requires building innovation systems and embracing creative destruction.

The only question is whether you will participate or stagnate.

by Robyn Bolton | Sep 30, 2025 | Leading Through Uncertainty, Strategy, Tips, Tricks, & Tools

Just as we got used to VUCA (volatile, uncertain, complex, ambiguous) futurists now claim “the world is BANI now.” BANI (brittle, anxious, nonlinear, incomprehensible) is much worse than VUCA and reflects “the fractured, unpredictable state of the modern world.”

Not to get too Gen X on the futurists who coined and are spreading this term but…shut up.

Is the world fractured and unpredictable? Yes.

Does it feel brittle? Are we more anxious than ever? Are things changing at exponential speed, requiring nonlinear responses? Does the world feel incomprehensible? Yes, to all.

Naming a problem is the first step in solving it. The second step is falling in love with the problem so that we become laser focused on solving it. BANI does the first but fails at the second. It wallows in the problem without proposing a path forward. And as the sign says, “Ain’t nobody got time for this.”

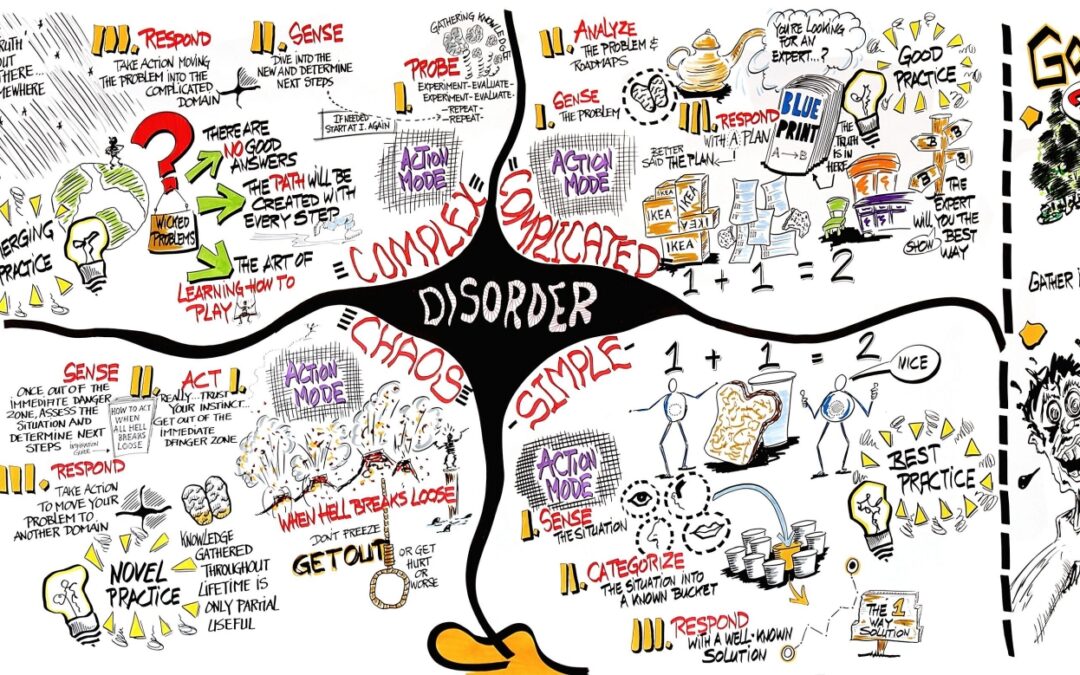

(Re)Introducing the Cynefin Framework

The Cynefin framework recognizes that leadership and problem-solving must be contextual to be effective. Using the Welsh word for “habitat,” the framework is a tool to understand and name the context of a situation and identify the approaches best suited for managing or solving the situation.

It’s grounded in the idea that every context – situation, challenge, problem, opportunity – exists somewhere on a spectrum between Ordered and Unordered. At the Ordered end of the spectrum, cause and affect are obvious and immediate and the path forward is based on objective, immutable facts. Unordered contexts, however, have no obvious or immediate relationship between cause and effect and moving forward requires people to recognize patterns as they emerge.

Both VUCA and BANI point out the obvious – we’re spending more time on the Unordered end of the spectrum than ever. Unlike the acronyms, Cynefin helps leaders decide and act.

5 Contexts. 5 Ways Forward

The Cynefin framework identifies five contexts, each with its own best practices for making decisions and progress.

On the Ordered end of the spectrum:

- Simple contexts are characterized by stability and obvious and undisputed right answers. Here, patterns repeat, and events are consistent. This is where leaders rely on best practices to inform decisions and delegation, and direct communication to move their teams forward.

- Complicated contexts have many possible right answers and the relationship between cause and effect isn’t known but can be discovered. Here, leaders need to rely on diverse expertise and be particularly attuned to conflicting advice and novel ideas to avoid making decisions based on outdated experience.

On the Unordered end of the spectrum:

- Complex contexts are filled with unknown unknowns, many competing ideas, and unpredictable cause and effects. The most effective leadership approach in this context is one that is deeply uncomfortable for most leaders but familiar to innovators – letting patterns emerge. Using small-scale experiments and high levels of collaboration, diversity, and dissent, leaders can accelerate pattern-recognition and place smart bets.

- Chaos are contexts fraught with tension. There are no right answers or clear cause and effect. There are too many decisions to make and not enough time. Here, leaders often freeze or make big bold decisions. Neither is wise. Instead, leaders need to think like emergency responders and rapidly response to re-establish order where possible to bring the situation into a Complex state, rather than trying to solve everything at once.

The final context is Disorder. Here leaders argue, multiple perspectives fight for dominance, and the organization is divided into fractions. Resolution requires breaking the context down into smaller parts that fit one of the four previous contexts and addressing them accordingly.

The Only Way Out is Through

Our VUCA/BANI world isn’t going to get any simpler or easier. And fighting it, freezing, or fleeing isn’t going to solve anything. Organizations need leaders with the courage to move forward and the wisdom and flexibility to do so in a way that is contextually appropriate. Cynefin is their map.