by Robyn Bolton | May 5, 2026 | Leadership, Leading Through Uncertainty, Stories & Examples, Strategy

Sunday morning, my phone blew up. Thirty-three text messages. Most mornings, I have zero, so my first thought was “who died?”

The texts were about a death. Sort of.

Sloan Management Review died (ceased publication) and a group chat filled with academics, thought leaders, and consultants were having an absolute meltdown.

Knowing that my husband, an actual Sloan graduate, hadn’t yet seen the news, I broke it to him gently. “Okay,” he shrugged, not even glancing up from his phone.

This was in stark contrast to his reactions to the demise of Spirit Airlines (howling with laughter at the memes) and the resurrection of Allbirds as an AI company (thoughtful and incredibly technical analysis).

Lesson 1: The Race to the Bottom Never Ends Well

CNN’s headline said it all, “Why did Spirit fail? Too many passengers hated flying it.” To prove the point, the article opens,

“Lousy service, not the Iran war, killed Spirit Airlines. Spirit was doomed to fail because of mismanagement, deep financial problems, and – crucially – its reputation for poor customer service. The spike in jet fuel prices during the war just accelerated Spirit’s inevitable demise.”

If that can be written about your business, you don’t deserve to be in business.

It’s only a matter of time until you’re not.

Lesson 2: Be Patient for Growth and Impatient for Profit

Allbirds raised $348 million when it IPOed in 2021 and, at one point, was valued at $4.1 billion despite never turning a profit. Six years later, its stock price had fallen 95% and it sold its business and IP to a brand management company for $39 million.

How did this happen? There are plenty of theories – it expanded too aggressively into bricks and mortar retail, it made ugly shoes but operated like a fashion brand, its Tech Bro image is no longer aspirational for Gen Z customers – but the fact is that it prioritized growth over profit and that ultimately bit them in the balance sheet.

Lesson 3: Some Businesses are Butterflies

While my colleagues’ alarm was understandable, it missed the bigger picture.

Sloan Management Review (SMR) didn’t die. It metamorphosed.

Yes, the SMR brand is going away, but future ideas, research and findings will continue to be shared through digital newsletters, short-form videos, podcasts, and social-first content.

In effect, SMR is metamorphosing to better reflect how its subscribers consume information. Busy executives don’t have the time to read long-form, dense research articles. They grab information in snippets and soundbites. This change ensures the people who need the ideas the most get them.

3 Questions to Find Your Fate

- Do you treat your customers like they exist for your benefit? In other words, are you more focused on value extraction than value creation and delivery? If yes, start planning your business’ funeral and don’t expect anyone to attend.

- Do you have a financially and operationally sustainable business model? If no, start planning your funeral but take comfort in the fact that people will attend and may even say nice things about you.

- Do you know the unique, relevant, valuable, and hard to imitate reason why you exist? Can you articulate the rare and essential Job to be Done you do for your customers? If no, you’re on life support. When you can answer yes, you’ll be ready to be a butterfly.

One quick caveat

When businesses die, people lose their jobs and that is incredibly tragic. The psychological, financial, and relational impacts of job loss are tremendous, impacting people far beyond the individual laid off. It can take months, even years for people and families to recover and, for some, it never happens.

Creative destruction is real and necessary for long-term economic, technological, and societal growth. But the short-term impact has human consequences that should never be ignored.

by Robyn Bolton | Feb 23, 2026 | Leadership, Stories & Examples, Strategy

Congratulations, you’ve done the hard part required to get buy-in! You asked instead of told, said “I don’t know” out loud, and got genuine buy-in. Your team believes, is engaged, and ready to go. And yet execution is stalling.

What gives?

Activity without Achievement

There’s no doubt that people are working hard. You can see it in their schedules and you hear it in your one-on-ones. But projects are moving slower than they should, decisions that seem straightforward take weeks, and agreements made in meetings are quietly undone. Strategies, buy-in, timelines are powerless against an invisible and unnamed force.

So, you consider your options. A team offsite can provide a helpful rest but there’s no guarantee it sticks when you’re back in the office. Training can help shore up skill gaps, but your team is already capable, so this doesn’t feel like a skill problem. You could reorg but that creates new problems.

Your People Aren’t the Problem

The problem isn’t your people, your team, or even your culture. The problem is the hidden seams between people, teams, and cultures, that create friction.

Because of friction, people hesitate to share information across functional or hierarchical seams. They make assumptions about other generations. They work to achieve individual or functional, rather than collective, goals.

These friction points have been part of your organization for so long that they are accepted as normal. As immoveable and unchangeable as your company’s mission and vision. And because they’re so ingrained, you shift your efforts to things that feel changeable: skills, org charts, and communication plans.

You’re addressing symptoms because the root cause seems impossible to fix.

It’s not impossible.

How One Company Resolved the Friction and Tightened the Seams Without Extra Work

When a K-5 curriculum company decided to expand into the Middle School market, they knew they were asking the project team to do something new that was complex, ambiguous, and fraught with high-stakes decisions.

Six months in, the project was breaking down. Decisions that should have taken a day took weeks or months. Work got stuck as different functions weighed in at different times with different mandatory requirements. People hid problems and gave optimistic updates.

The executive who owned the project had seen this before. In fact, she was seeing it in every project team across the entire company. So, she knew that the problem wasn’t the project or the people, it was something much deeper, something that was such a part of the company’s standard operating process that it had become invisible.

So, she brought in someone (me) who could see things differently and together we sought out the seams, naming the moments when friction occurred, and engaging the team in developing and experimenting with solutions.

And we did it all as part of the daily work.

We redesigned hand-offs in real time, experimented with decision-making rules until we found what worked for multiple decision types, and rewarded people for saying “I don’t know.”

Within six months, the project was back on track and engagement and morale were sky-high. Other teams took notice and asked for advice. New products began shipping on time, on budget, and to rave reviews.

Now the Real Work Begins

Where are your seams showing up? A cross-functional initiative that’s losing momentum? A decision that never seems to stick? A team that’s aligned on paper but stuck in execution?

That friction has a name. And it’s findable.

If you’re ready to find the seams and resolve the friction, set up a SeamSpotter Session. It’s a 60 to 90-minute conversation, no prep required, and you’ll receive a written summary and recommended next steps within 48 hours.

If your team is bought in, but execution keeps stuttering, you can fix it. Email me at robyn@milezero.io to get started.

by Robyn Bolton | Jan 17, 2026 | AI, Leadership, Leading Through Uncertainty, Stories & Examples

You’ve clarified the vision and strategy. Laid out the priorities and simplified the message. Held town halls, answered questions, and addressed concerns. Yet the AI initiative is stalled in ‘pilot mode,’ your team is focused solely on this quarter’s numbers, and real change feels impossible. You’re starting to suspect this isn’t a “change management” problem.

You’re right. It’s not.

The Data You’re Not Seeing

You’ve been doing what the research tells you to do: communicate clearly and frequently, clarify decision rights, and reduce change overload. And these things worked. Until employees went from grappling with two to 10 planned change initiatives in a single year. As the number went up, willingness to support organization change crashed, falling from 74% of employees in 2016 to 43% in 2022.

But here’s what the research isn’t telling you: despite your organizational fixes, your people are terrified. 77% of workers fear they’ll lose their jobs to AI in the next year. 70% fear they’ll be exposed as incompetent. And 66% of consumers, the highest level in a decade, expect unemployment to continue to rise.

Why doesn’t the research focus on fear? Because it’s uncomfortable. Messy. It’s a people (Behavior) problem, not a process (Architecture) problem and, as a result, you can’t fix it with a new org chart or better meeting cadence.

The organizational fixes are necessary. They’re just not sufficient to give people the psychological reassurance, resilience, and tools required to navigate an environment in which change is exponential, existential, and constant.

What Actually Works

In 2014, Microsoft was toxic and employees were afraid. Stack ranking meant every conversation was a competition, every mistake was career-limiting, and every decision was a chance to lose status. The company was dying not from bad strategy, but from fear.

CEO Satya Nadella didn’t follow the old change management playbook. He did more:

First, he eliminated the structures that created fear, including the stack ranking system, the zero-sum performance reviews, the incentives that punished mistakes. These were Architecture fixes, and they mattered.

And he addressed the messy, uncomfortable emotions that drove Behavior and Culture. He role modeled the Behaviors required to make it psychologically safe to be wrong. He introduced the “growth mindset” not as a poster on the wall, but as explicit permission to not have all the answers. When he made a public gaffe about gender equality, he immediately emailed all 200,000 employees: “My answer was very bad.” No spin. No excuses. Just modeling the vulnerability that he expected from everyone.

Ten years later, Microsoft is worth $2.5 trillion. Employee engagement and morale are dramatically improved because Nadella addressed the structures that fed fear AND the fear itself.

What This Means for You

You don’t need to be Satya Nadella. But you do need to stop pretending fear doesn’t exist in your organization.

Name it early and often. Not just in the all-hands meeting, but in the team meetings and lunch-and-learns. Be honest, “Some roles will change with this AI implementation. Here’s what we know and don’t know.” Make the implicit explicit.

Eliminate the structures that create fear. If your performance system pits people against each other, change it. If people get punished for taking smart risks, stop. If people ask questions or make suggestions, listen and act.

Be vulnerable. Share what you’re uncertain about. Admit when you don’t know. Show that it’s safe to be learning. Demonstrate that learning is better than (pretending to) know.

The stakes aren’t abstract: That AI pilot stuck in testing. The strategic initiative that gets compliance but not commitment. The team so focused on surviving today they can’t prepare for tomorrow. These aren’t communication failures. They’re misaligned ABCs that allow fear to masquerade as pragmatism.

And the masquerade only stops when you align align the ABCs all at once. Because fixing Architecture without changing your Behavior simply gives fear a new place to hide.

by Robyn Bolton | Nov 19, 2025 | Innovation, Stories & Examples

I can’t believe that I’m writing this. Honestly, I can’t believe I’m even thinking this. I’m an open-minded person, but I truly never thought that anything would ever change my mind on this topic. And yet, I must confess that I’ve come to the conclusion that…

(deep breath)

Innovation Theater is important.

(Sorry, needed a minute to recover. It’s one thing to think something. It’s another to see it in writing.)

Why We All Hate(d) Innovation Theater.

The term “Innovation Theater” was coined by Steve Blank in a 2019 HBR article to describe innovation activities like hackathons, shark tanks, and workshops that “shape and build culture, but they don’t win wars, and they rarely deliver shippable/deployable product.”

The name stuck because it gave the Innovation Industrial Complex a perfect scapegoat. Innovation efforts weren’t producing results because companies were turning real strategy into theater—events that could be delegated and scheduled instead of the courage, commitment, and willingness to change that actual innovation requires.

And in many cases, this criticism was warranted.

But in our rush to dismiss Innovation Theater, we missed something important.

What I (Almost) Missed.

Recently, I visited a company’s Innovation Center, curious to see what ten years of innovation investments and two floors in a downtown high-rise had produced.

The answer was a framework to think more deeply about equity and inclusion. My immediate reaction was rage. A decade of investments for this? Millions of dollars spent on the very definition of Innovation Theater? And they’re bragging about it?!?

Once the rage subsided, something remained. Something that I couldn’t shake. An inkling that I had missed something. That inkling became the realization that I was wrong.

Over the past five years, the framework had been used in carefully curated workshops to help teams across the organization see things they had previously overlooked, understand topics that were sensitive or taboo, and envision solutions that no one their heavily regulated industry had even considered.

Not every workshop resulted in action. But over time, something shifted.

Seasons. Not Shows.

Repetition created a shared language. Multiple touchpoints built permission. Small success stories accumulated to make risk feel manageable. The workshops didn’t send off isolated sparks of innovation. They built the conditions were acting on new ideas became progressively safer and more normal.

And after several seasons, enduring value was created. The company now enjoys the highest retention rate of customers in its industry and has attracted more new customers than all its competitors combined. A decade of “Innovation Theater” delivered exactly what innovation is supposed to deliver: measurable competitive advantage and revenue growth.

Don’t Cancel Your Next Innovation Event.

The problem isn’t Innovation Theater itself. It’s how we practice it.

A one-off hackathon? Theater. An annual workshop? Theater. But sustained investment over years, touching dozens of teams, building shared language and accumulated proof points? That’s a strategic bet on transformation that creates lasting competitive advantage.

The question isn’t whether Innovation Theater works. It’s whether you’re willing to commit to the season, not just the show. Are you prepared to invest consistently, measure differently, and wait for compounding effects that won’t show up in next quarter’s results?

Because when you commit to the season, not just the show, it’s the most strategic bet you can make.

by Robyn Bolton | Aug 4, 2025 | Leadership, Leading Through Uncertainty, Stories & Examples, Strategy

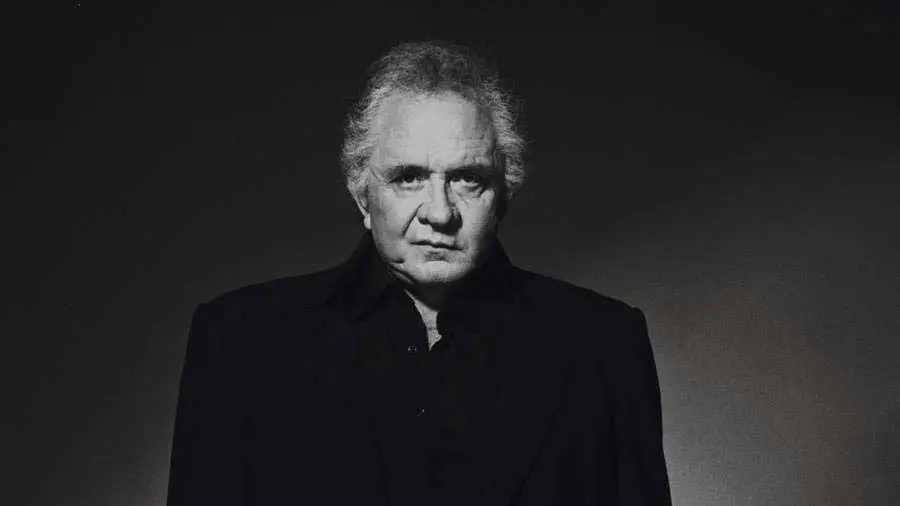

The best business advice can destroy your business. Especially when you follow it perfectly.

Just ask Johnny Cash.

After bursting onto the scene in the mid-1950s with “Folsom Prison Blues”, Cash enjoyed twenty years of tremendous success. By the 1970s, his authentic, minimalist approach had fallen out of favor.

Eager to sell records, he pivoted to songs backed by lush string arrangements, then to “country pop” to attract mainstream audiences and feed the relentless appetite of 900 radio stations programming country pop full-time.

By late 1992, Johnny Cash’s career was roadkill. Country radio had stopped playing his records, and Columbia Records, his home for 25 years, had shown him the door. At 60, he was marooned in faded casinos, playing to crowds preferring slot machines to songs.

Then he took the stage at Madison Square Garden for Bob Dylan’s 30th anniversary concert.

In the audience sat Rick Rubin, co-founder of Def Jam Recordings and uber producer behind Public Enemy, Run-DMC, and Slayer, amongst others. He watched in awe as Cash performed, seeing not a relic but raw power diluted by smart decisions.

The Stare-Down that Saved a Career

Four months later, Rubin attended Cash’s concert at The Rhythm Café in Santa Anna, California. According to Cash’s son, “When they sat down at the table, they said: ‘Hello.’ But then my dad and Rick just sat there and stared at each other for about two minutes without saying anything, as if they were sizing each other up.”

Eventually, Cash broke the silence, “What’re you gonna do with me that nobody else has done to sell records for me?”

What happened next resurrected his career.

Rubin didn’t promise record sales. He promised something more valuable: creative control and a return to Cash’s roots.

Ten years later, Cash had a Grammy, his first gold record in thirty years, and CMA Single of the Year for his cover of Nine Inch Nails’ “Hurt,” and millions in record sales.

When Smart Decisions Become Fatal

Executives do exactly what Cash did. You respond to market signals. You pivot your offering when customer preferences shift and invest in emerging technologies.

All logical. All defensible to your board. All potentially fatal.

Because you risk losing what made you unique and valuable. Just as Cash lost his minimalist authenticity and became a casualty of his effort to stay relevant, your business risks losing sight of its purpose and unique value proposition.

Three Beliefs at the Core of a Comeback

So how do you avoid Cash’s initial mistake while replicating his comeback? The difference lies in three beliefs that determine whether you’ll have the creative courage to double down on what makes you valuable instead of diluting it.

- Creative confidence: The belief we can think and act creatively in this moment.

- Perceived value of creativity: Our perceived value of thinking and acting in new ways.

- Creative risk-taking: The willingness to take the risks necessary for active change.

Cash wanted to sell records, and he:

- Believed that he was capable of creativity and change.

- Saw the financial and reputational value of change

- Was willing to partner with a producer who refused to guarantee record sales but promised creative control and a return to his roots.

Your Answers Determine Your Outcome

Like Cash, what you, your team, and your organization believe determines how you respond to change:

- Do I/we believe we can creatively solve this specific challenge we’re facing right now?

- Is finding a genuinely new approach to this situation worth the effort versus sticking with proven methods?

- Am I/we willing to accept the risks of pursuing a creative solution to our current challenge?”

Where there are “no’s,” there is resistance, even refusal, to change. Acknowledge it. Address it. Do the hard work of turning the No into a Yes because it’s the only way change will happen.

The Comeback Question

Cash proved that authentic change—not frantic pivoting—resurrects careers and disrupts industries. His partnership with Rubin succeeded because he answered “yes” to all three creative beliefs when it mattered most. Where are your “no’s” blocking your comeback?

by Robyn Bolton | Jul 23, 2025 | Leadership, Leading Through Uncertainty, Stories & Examples

What does a lightning strike in a Spanish forest have to do with your next leadership meeting? More than you think.

On June 14, 2014, lightning struck a forest on Spain’s northeast coast, only 60 miles from Barcelona. Within hours, flames 16 to 33 feet high raced out of control toward populated areas, threatening 27,000 acres of forest, an area larger than the city of Boston.

Everything – data, instincts, decades of firefighting doctrine – prioritized saving the entire forest and protecting the coastal towns.

Instead, the fire commanders chose to deliberately let 2,057 acres, roughly the size of Manhattan’s Central Park, burn.

The result? They saved the other 25,000 acres (an area the size of San Francisco), protected the coastal communities, and created a natural firebreak that would protect the region for decades. By accepting some losses, they prevented catastrophic ones.

The Fear Trap That’s Strangling Your Business

The Tivissa fire’s triumph happened because firefighters found the courage to escape what researchers call the “fear trap” – the tendency to focus exclusively on defending against known, measurable risks.

Despite research proving that defending against predictable, measurable risks through defensive strategies consistently fails in uncertain and dynamic scenarios, firefighter “best practices” continue to advocate this approach.

Sound familiar? It should. Most executives today are trapped in exactly this pattern.

We’re in the fire right now. Financial markets are yo-yoing, AI threatens to disrupt everything, and consumer behaviors are shifting.

Most executives are falling into the Fear Trap by doubling down on protecting their existing business and pouring resources into defending against predictable risks. Yet the real threats, the ones you can’t measure or model, continue to pound the business.

While you’re protecting last quarter’s wins, tomorrow’s disruption is spreading unchecked.

Four Principles for Creative Decision-Making Under Fire

The decision to cede certain areas wasn’t hasty but based on four principles enabling leaders in any situation to successfully navigate uncertainty.

PRINCIPLE 1: A Predictable Situation is a Safe Situation. Stop trying to control the uncontrollable. Standard procedures work in predictable situations but fail in unprecedented challenges.

Put it in Practice: Instead of creating endless contingency plans, build flexibility and agility into operations and decision-making.

PRINCIPLE 2: Build Credibility Through Realistic Expectations. Reducing uncertainty requires realism about what can be achieved. Fire commanders mapped out precisely which areas around Tivissa would burn and which would be saved, then communicated these hard truths and the considered trade-offs to officials and communities before implementing their strategy, building trust and preventing panic as the selected areas burned.

Put it in practice: Stop promising to protect everything and set realistic expectations about what you can control. Then communicate priorities, expectations, and trade-offs frequently, transparently, and clearly with all key stakeholders.

PRINCIPLE 3: Include the future in your definition of success: Traditional firefighting protects immediate assets at risk. The Tivissa firefighters expanded this to include future resilience, recognizing that saving everything today could jeopardize the region tomorrow.

Put it in practice: Be transparent about how you define the Common Good in your organization, then reinforce it by making hard choices about where to compete and where to retreat. The goal isn’t to avoid all losses – it’s to maximize overall organizational health.

PRINCIPLE 4: Use uncertainty to build for tomorrow: Firefighters didn’t just accept that 2,057 acres would burn – they strategically chose which acres to let burn to create maximum future advantage, protecting the region for generations.

Put it in practice: Evaluate every response to uncertainty on whether it better positions you for future challenges. Leverage the disruption to build capabilities, market positions, and organizational structures that strengthen you for future uncertainty.

Your Next Move

When the wind shifted and the fire exploded, firefighters had to choose between defending everything (and likely losing it all) or accepting strategic losses to ensure overall wins.

You’re facing the same choice right now.

Like the firefighters, your breakthrough might come not from fighting harder against uncertainty, but from learning to work with it strategically.

What are you willing to let burn to save what matters most?